In light of the recent attention drawn to mRNA-based vaccines, it is crucial to recognize that the groundwork for this pioneering technology has been laid over the course of more than three decades, as recognised by the 2023 Nobel Prize in Medicine and Physiology.

The journey began with the discovery of mRNA in the early 1960s, prompting scientists to pioneer its use in directing cells to produce viral components, thereby enhancing the immune response. Simultaneously, in the private sector, biotechnology companies in Canada delved into the emerging field of gene therapy, specifically aiming to protect “fragile” genetic molecules for secure delivery into human cells. Another pivotal trajectory emerged in the 1990s when the US government initiated a substantial investment to develop a vaccine against AIDS. Although an HIV vaccine remained elusive, this research inadvertently provided insights crucial for mapping coronavirus spikes.

The culmination of these endeavors manifested during the COVID-19 pandemic, catalyzing the rapid development and approval of the first mRNA vaccines, Pfizer-BioNTech’s Comirnaty and Moderna’s SpikeVax. These scientific breakthroughs, combined with the validated safety and efficacy of mRNA demonstrated through the administration of billions of vaccine doses, have unveiled the potential for mRNA to serve as both therapeutics and vaccines across a multitude of indications.

Unremarkable benefits of mRNA technology

Messenger RNA, or mRNA, exists in all of our cells and is an essential component of all living organisms. Just as its name suggests, mRNA acts as a messenger, carrying instructions to produce specific proteins that can bolster the immune system’s ability to prevent or treat certain diseases.

But what makes mRNA truly revolutionary is its modular nature, which sparks a paradigm shift in medicine production. From a manufacturing and development standpoint, the mRNA’s modular nature brings a myriad of advantages to other methods for medicine production.

In particular, as mRNA harnesses our cellular system to make proteins based on the instructions provided by mRNA’s genetic code, it bypasses the need for costly manufacturing of proteins in fermentation tanks. In other words, the mRNA uses the human body as its own vaccine or drug production facility. Furthermore, unlike small molecule and protein-based drug substances, mRNA can be tailored to encode almost any protein while retaining nearly the same chemical characteristics due to the flexibility of the platform, which allows for swift design and customization. To put things into perspective, Moderna finalized the sequence of the mRNA-1273 COVID-19 vaccine in just 2 days, following the release of the virus sequence, and only 25 days were needed to manufacture the first clinical batch. This is an incredible achievement, given that conventional vaccine development typically spans 8-14 years. Finally, mRNA products are relatively easy to redesign, which is especially useful from the perspective of pandemic preparedness, where a vaccine can be adapted to a new viral strain within days of its identification.

Another significant advantage is that mRNA manufacturing requires a small facility footprint. To illustrate, a 5 L bioreactor can produce 100 M doses of mRNA drug substance annually. This efficiency stems from using a cell-free, highly efficient, and scalable synthetic biochemical process, which involves utilizing an enzyme, RNA polymerase, to synthesize mRNA drug substance based on a DNA template. In stark contrast, manufacturing cell-based products, including recombinant proteins or viruses for conventional vaccines, requires large and capital-intensive facilities equipped with 2000 L reactors. The production is highly complex and notably slower, with the upstream and mid-stream processes taking up to several months. In terms of economics, the estimated capital cost for a facility to produce 100 M doses of mRNA vaccines is $14M, presenting a favorable comparison to an equivalent-capacity virus-based vaccine facility, which demands an investment ranging from $50M to $60M. This showcases the efficiency and resource-friendly nature of mRNA manufacturing, making it a particularly appealing option for pharmaceutical production.

Hurdles to overcome

The rapid response to the pandemic was undoubtedly facilitated by mRNA technology, showcasing its potential in both vaccines and therapeutics.

It is important to note that mRNA therapeutics face distinct challenges that go beyond the scope of vaccine development. The primary drawback lies in the inherent immunogenicity of mRNA. While this characteristic boosts its effectiveness as a vaccine, it hinders its application as a therapeutic. Moreover, therapeutic use requires roughly a 1000-fold higher protein level to reach the therapeutic threshold. This poses a significant challenge, particularly in treating chronic diseases that require repeated dosing, increasing the likelihood of activating innate immunity and resulting in lower protein expression.

Another major hurdle lies in lacking an mRNA delivery system capable of targeting organs of interest, a critical step in addressing certain diseases. Although lipid nanoparticles [LNPs] have undergone extensive testing as mRNA delivery vehicles for IM administration, particularly in vaccines, their limited tropism currently restricts their use to the liver. As a result, alternative RoAs, such as skin patches, and oral and inhaled formulations, are currently being explored for both vaccine and drug delivery through public-private partnerships such as BARDA’s “Beyond the Needle” R&D program.

Furthermore, despite the surge in demand for mRNA manufacturing services during the COVID-19 pandemic, which placed immense pressure on Contract Development and Manufacturing Organizations (CDMOs), current initiatives by mRNA players to enhance their in-house mRNA production signal a transition towards internalizing manufacturing rather than relying solely on external contractors. This shift is particularly relevant in anticipation of potential upcoming vaccine and therapeutic approvals.

Another major challenge was related to securing a stable supply of essential raw materials, including plasmids necessary for mRNA transcription and lipids crucial for mRNA delivery. To address this, leading manufacturing companies in the domain, such as Thermo Fisher Scientific, Charles River Laboratories, and Aldevron, have undertaken various expansion efforts. These include the development and implementation of novel and more efficient operating protocols, as well as the optimization of the current plasmid production process.

Lastly, the instability of mRNA vaccines, which currently require cold (-20 °C) or ultracold (-80 °C) storage conditions, posed a significant hurdle for the supply chain and global distribution. In fact, the high cost of mRNA vaccines compared to traditional vaccines is largely attributed to supply-side challenges, limiting access predominantly to developed countries. However, mRNA-based vaccines in development for tropical diseases receive substantial support from multilateral organizations (e.g., CEPI, WHO).

Big pharma bet on mRNA-based vaccines

In the post-pandemic era, the landscape of mRNA-based medicines in clinical development has significantly expanded, including preventive and therapeutic mRNA vaccines and therapeutics. Beyond COVID-19, mRNA modality is being applied for various therapeutic areas, with infectious diseases, oncology, and lung diseases being among the most commonly pursued indications by key mRNA players and large pharmaceutical companies.

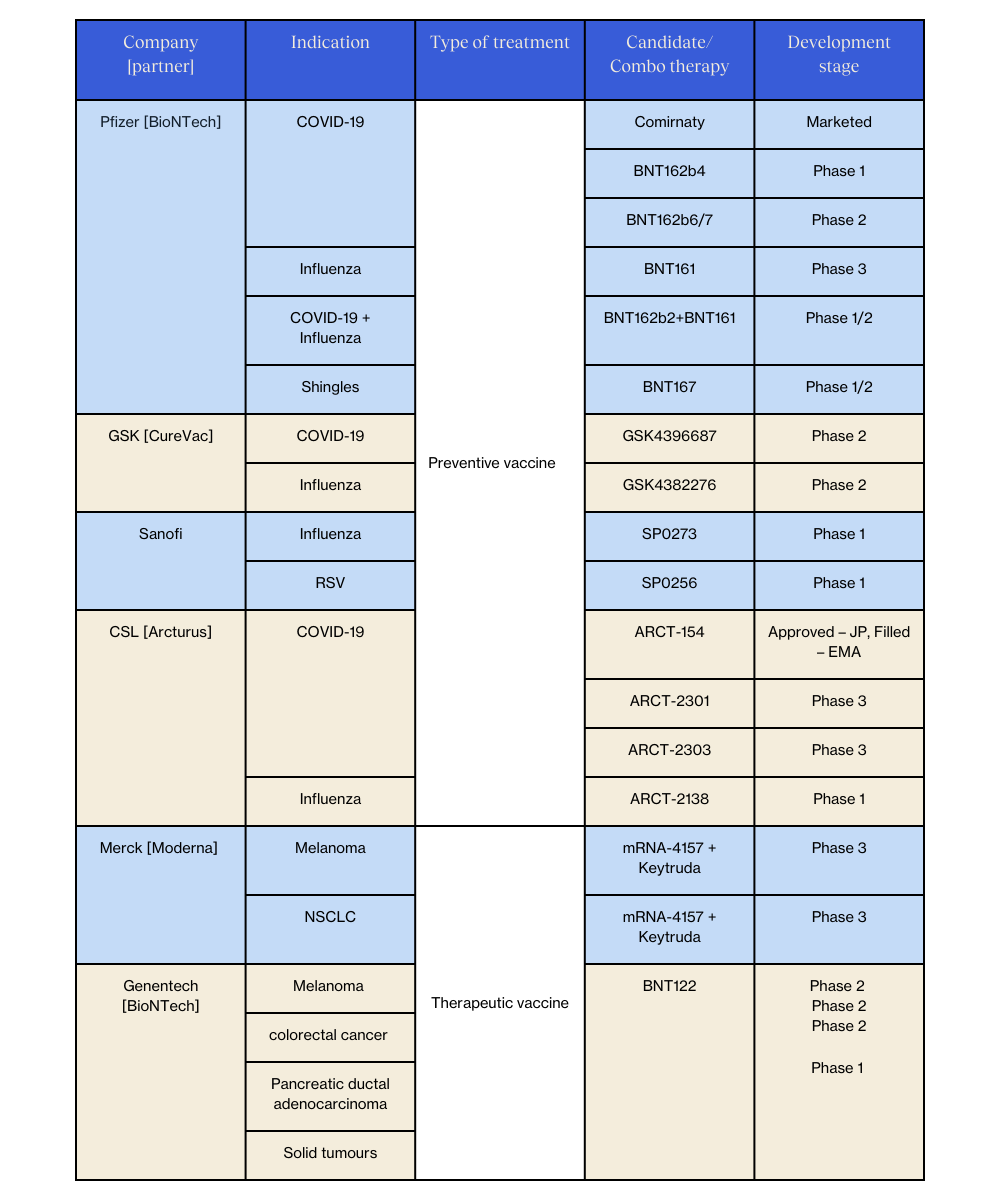

Notably, start-ups with proprietary mRNA platforms continue to dominate when considering the number of mRNA assets in development compared to large pharma companies. Key players in this space include Moderna, BioNTech, CureVac, Arcturus, and Gristone. When examining pipelines, vaccines are the leaders, constituting 80% of Moderna’s and 56% of BioNTech’s assets (Apr 2024). This emphasis on vaccines is attributed to the lower investment risk associated with the development, given the validated platform in a real-world setting, whereas therapeutic development, requiring roughly a 1000-fold higher protein level to reach the therapeutic threshold, poses heightened challenges.

Large pharmaceutical companies have also incorporated mRNA-based assets into their pipelines. Pfizer, Sanofi, GSK, CSL, Roche, and Merck are among the major players venturing into mRNA technology [see table below]. Particularly, vaccine giants such as Pfizer, Sanofi, GSK, and CSL demonstrate a keen interest in investing in preventive mRNA vaccine programs, aligning with the strategies of mRNA start-up companies. At the same time, Merck and Roche/Genentech, maintaining their emphasis on therapeutic applications, have integrated mRNA initiatives directed towards therapeutic vaccines into their portfolio.

However, it is important to note that all these mRNA pipeline additions are not very significant and rather moderate, ranging from two to five candidates compared to other modalities in similar indications. This moderate scale suggests that companies are broadening their pipeline by including various modalities, rather than depending solely on mRNA candidates.

For the development of mRNA assets, most large pharmaceutical companies opt for partnerships with innovative startups. Among these collaborations, the Pfizer- BioNTech alliance stands out as one of the most recognized, featuring five ongoing mRNA vaccine programs, including flu and shingles, along with a novel combination vaccine targeting both flu and COVID-19. Meanwhile, other vaccine giants like GSK and CSL collaborate with CureVac and Arcturus, respectively, with programs focused on prophylactic vaccines against flu and COVID-19. In contrast, Sanofi has adopted a bolder strategy to expedite the development of mRNA assets. This involved the acquisition of the mRNA-specializing startup TranslateBio and establishing an in-house mRNA Centre of Excellence for advancement of vaccines and therapeutics. Sanofi has two active mRNA vaccine trials, evaluating RSV and flu candidates.

In terms of therapeutic vaccines, today, these primarily aim at cancer treatment. Merck has two ongoing ventures with Moderna, evaluating a combination therapy involving an investigational personalized mRNA vaccine, mRNA-4157, and Keytruda. This combination is being explored for the treatment of melanoma and non-small cell lung cancer [NSCLC], both currently in Ph3. Although these programs are viewed as promising [with positive Ph2b data in melanoma presented in Dec 2023], the therapy is expected to be available in the market beyond 2030, potentnially as part of Keytruda’s life cycle management.

Lastly, Genentech and BioNTech are also collaborating on the development of a personalized therapeutic vaccine, BNT122. This asset is investigated for use as a monotherapy against colorectal cancer or in combination therapies, with Keytruda for melanoma, and with Tecentriq for pancreatic ductal adenocarcinoma [PDAC] or multiple solid tumors. These programs are in early-stage development, ranging from early Ph1 to late Ph2, and are anticipated to hit the market beyond 2026.

Notably, Moderna had also teamed up with Vertex Pharmaceuticals to identify and develop LNPs and mRNAs for the delivery of gene-editing therapies to treat cystic fibrosis.

While these large pharma companies solidify their partnerships with ongoing clinical trials, additional vaccine players are gearing up to introduce mRNA assets into their pipelines. AstraZeneca, for instance, signed an agreement in H2 2023 with CanSino, a Chinese CDMO, which will provide manufacturing services to support the Anglo-Swedish drug maker’s early-stage mRNA vaccines and monoclonal antibodies against infectious diseases.

In general, preventive vaccines against infectious diseases are more numerous and advanced in clinical development than their therapeutic counterparts, with multiple assets in pivotal trials. The next wave of approvals for mRNA vaccines is anticipated in 2024-2025, including flu, RSV and novel flu + COVID-19 combo products.

Figure 1: Active mRNA clinical development programs of large pharma companies, conducted alone or with external partners.

So what’s next?

The journey from decades of research to the rapid development of mRNA-based vaccines during the COVID-19 pandemic marks just the beginning of this revolutionary technology’s potential. As we look ahead, the next phase promises even greater strides and innovations.

While current focus primarily lies in infectious disease prevention, the robust nature of mRNA technology is propelling its expansion into therapeutic realms. Leader companies such as Moderna and BioNTech are spearheading efforts to broaden its applications, with a plethora of programs exploring therapeutic vaccines and treatments across diverse medical domains.

With large pharma companies currently testing the waters for their mRNA pipeline additions, increased investment is expected over the next 5 years, especially in the therapeutic space. This shift will be attributed to the awaited positive results from the advanced clinical programs evaluating therapeutics and therapeutic vaccines. If this goes well, mRNA medicines are projected to be a lucrative business, with BioNTech founders Ozlem Tureci and Ugur Sahin suggesting that “in 15 years, one-third of all newly approved drugs will be based on mRNA”.

Despite the promising outlook, challenges persist on the manufacturing front. The rising demand for nucleic acid therapies, including mRNA, may strain existing manufacturing services, potentially leading to supply shortages. This underscores the need for further development and fortification of the supply chain infrastructure to meet the growing demand for mRNA-based medicines.

In essence, as mRNA technology continues to evolve and diversify, it stands poised to revolutionize the pharmaceutical industry, offering unparalleled opportunities for innovation, investment, and therapeutic advancement. The next chapter in the mRNA saga holds the promise of transforming the way we treat and prevent diseases, ushering in a new era of precision medicine and improved global health outcomes.